New Capital is part of EFG Asset Management. For more information visit: www.efg.com

House View

Inview April 2024

Editorial

Welcome to the April edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

The global equity market rally continued in March, with the MSCI World index posting a monthly gain of 3.3% and bringing performance in the first quarter of 2024 to 9.0%. Market leadership rotated from large tech companies to financials and small caps over the month. In fixed income, government bond yields were little changed and corporate bond spreads tightened further. Despite the US dollar rising moderately against the major currencies, the price of gold rose to a record high.

The last few weeks were dominated by central bank meetings. The Bank of Japan terminated its Negative Interest Rate policy, raising interest rates for the first time since 2007. In contrast, the Swiss National Bank cut interest rates. The Federal Reserve, European Central Bank and Bank of England all left interest rates unchanged but signalled that rate cuts are likely in the not-too-distant future. Markets reacted positively, focusing on the fact that financial conditions should become more accommodative rather than worrying about the uncertainty surrounding the timing and magnitude of policy easing.

The outlook for US monetary policy is uncertain. Markets anticipate three rate cuts in 2024, but Fed Chairman Jerome Powell kept all options open noting resilient economic growth and sticky inflation. The possibility that the Federal Reserve will cut rates later and by less than previously expected cannot be ruled out.

An improved growth outlook should provide support to risky assets but carries the risk of increased short-term volatility as markets adjust to the possibility of less accommodative monetary policy. With this in mind, and in view of recent equity market strength, a moderate overweight in equities seems advisable along with a slight underweight exposure to fixed income assets. Keeping some cash available will allow us to take advantage of any temporary correction.

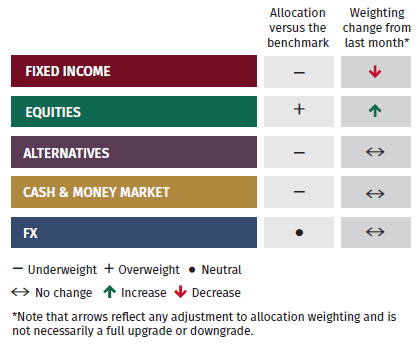

Asset Allocation

Global Allocation

Recent economic data releases have generally come in better than expected and we expect inflation to continue to fall over the coming months, painting a generally positive economic picture. However there remains uncertainty and it should be noted that the yield curve remains negatively sloped, pointing to potential challenges for the growth outlook. Global equities continued to outperform fixed income markets in March. Given equities have seen strong momentum, we are increasing our equity exposure whilst slightly downgrading fixed income positioning in line with market drift. This means that we retain our modest equity overweight position relative to the neutral allocation, while having a marginal underweight in fixed income. If the improving trend in equity earnings projections does not continue, we may need to consider the allocation due to current stretched valuations. Having raised cash the prior month, we are maintaining levels at a slight underweight as well as keeping our underweight allocation to alternatives.

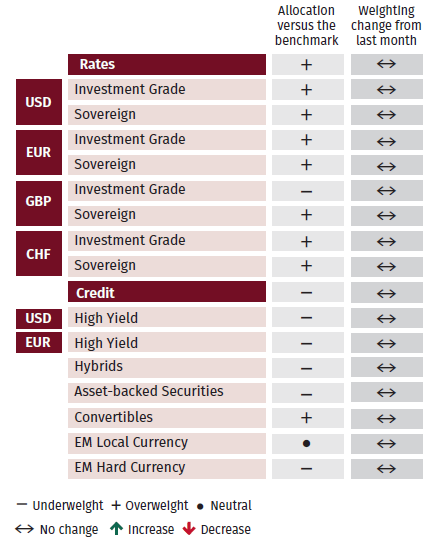

Fixed Income

In USD fixed income, we continue to hold an overweight allocation to both sovereign and investment grade (IG) bonds, given that spreads remain tight. The overweight is marginally larger for sovereign bonds in USD as IG corporate bond spreads are in the lower quartile of their historic range. The reverse is true in EUR, where we hold a slightly larger overweight in investment grade bonds relative to sovereign bonds. In GBP, there is a large overweight for sovereign bonds given the weakness in the UK economy, and in CHF, there is a positive skew towards investment grade bonds but less so to sovereigns, though both allocations are overweight relative to the benchmark. High yield bond spreads are still tight in USD and EUR currencies and so we remain underweight in these areas relative to the benchmark.

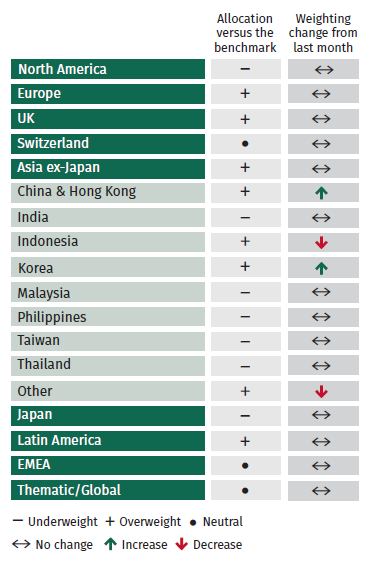

Equities

While our underweight Japan position has not yet paid off given the continued strength seen in the market, we are not making any adjustments for now, with valuations looking expensive. Another area we are watching closely is Latin America. This follows on from the move last month to increase our overweight stance. Technical factors will continue to be monitored but there may be potential for a catchup trade in the region given recent underperformance. Within Asia ex-Japan, Hong Kong exposure was slightly lifted as we see more signs in selective areas of a bottoming out. Korea exposure was raised to a modest overweight, looking for opportunities in areas of semi capex, cosmetics and aesthetics, where South Korean companies look well positioned in our view. Having reduced US exposure further underweight last month, we are making no changes this month but note that technical signals for all sectors are positive and there could be further upside on this basis. Last month we upgraded Swiss equities to neutral as valuations had become more attractive and there was the prospect of a rate cut from the Swiss National Bank, which did end up happening.

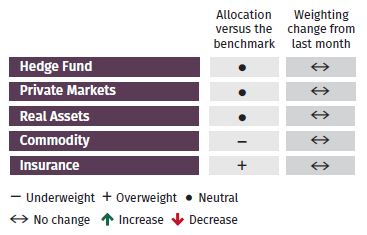

Alternatives

Hedge fund indices performance over twelve months highlights the strong returns of Equity Long/Short and Equity Market Neutral strategies. While overall we are neutral on Hedge Funds, within the sub-asset class we prefer equity-related strategies. The expectation of rising performance dispersion, the persistence of trending behaviour and a backdrop of uncertainty as we head into late 2024, are all features supportive of these strategies. Yields on cat bonds remain elevated with wide spreads relative to history, making this asset class attractive in our view. The insurance segment remains our preferred area of alternatives. We continue to hold an underweight allocation to commodities versus the benchmark.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

Independent Asset Managers: in case this document is provided to Independent Asset Managers (“IAMs“), it is strictly forbidden to be reproduced, disclosed or distributed (in whole or in part) by IAMs and made available to their clients and/or third parties. By receiving this document IAMs confirm that they will need to make their own decisions/judgements about how to proceed and it is the responsibility of IAMs to ensure that the information provided is in line with their own clients’ circumstances with regard to any investment, legal, regulatory, tax or other consequences. No liability is accepted by EFG for any damages, losses or costs (whether direct, indirect or consequential) that may arise from any use of this document by the IAMs, their clients or any third parties.

What type of investor are you?

to view the content you have selected, please choose your country/region and then investor type from the menu:

![]()

You’re about to leave EFGAM website and enter into a 3rd party website

Third party website disclaimer

You are about to enter a third party website, which is owned and operated by an independent party over which EFGAM has no control ("3rd Party Website"). Any link you make to or from the 3rd Party Website will be at your own risk. Any use of the 3rd Party Website will be subject to and any information you provide will be governed by the terms of the 3rd Party Website, including those relating to confidentiality, data privacy and security.

EFGAM does not endorse or approve and makes no warranties, representations or undertakings relating to the content of the 3rd Party Website. EFGAM disclaims liability for any loss, damage and any other consequence resulting directly or indirectly from or relating to your access to the 3rd Party Website or any information that you may provide or any transaction conducted on or via the 3rd Party Web site or the failure of any information, goods or services posted or offered at the 3rd Party Website or any error, omission or misrepresentation on the 3rd Party Website or any computer virus arising from or system failure associated with the 3rd Party Website.

By clicking "Proceed", you confirm that you have read and agreed to the terms herein.